Show

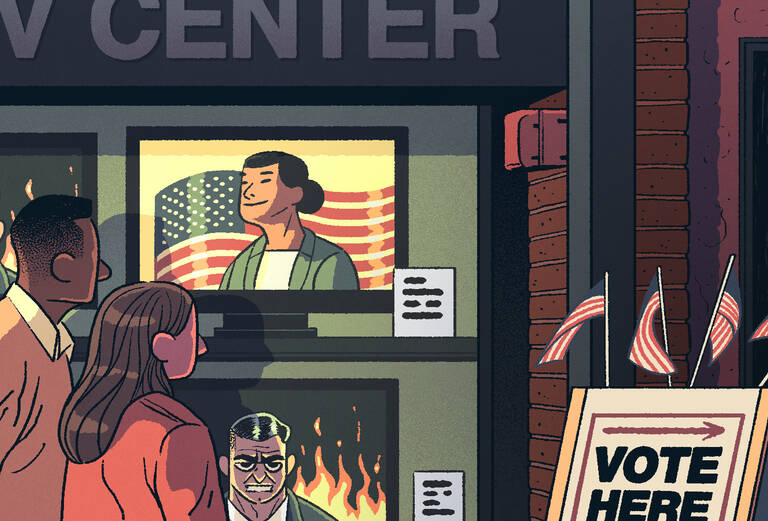

Are shareholders better off if they directly control corporate decisions? New research shows that answering this question requires considering numerous factors—and that intuitive answers are not always right. Artur Raviv, a professor of finance at the Kellogg School of Management, and Milton Harris, a professor at the University of Chicago, say that sometimes shareholders who lack information or are even misinformed should control decisions on matters on which management is better informed. The catch is that shareholders need recognize their blind spots and the extent of management’s private information. In theory, a corporation’s board of directors represents the interests of the shareholders. However, it is commonly believed that board members do not exercise sufficient control over self-interested managers because directors are typically handpicked by management insiders who control the proxy process. Raviv explains, “Eventually a conflict develops between the shareholders, who are the owners of the corporation, and the management, which is supposed to represent them, and the board, which is supposed to be supervising management.” The conflict has given rise to the “shareholder democracy movement,” in which many stock owners seek a greater voice in corporate decision-making. Gaining MomentumSome prominent examples of this movement have made headlines. Carl Icahn was unsuccessful in forcing a breakup of Time Warner, but he won concessions in exchange for dropping his proxy fight. Although Kirk Kerkorian succeeded in placing his representative on the board of General Motors, he was unable to compel GM to enter into an alliance with Nissan and Renault. On the other hand, Nelson Peltz succeeded in getting himself and an ally elected to the board of H.J. Heinz Co. and in persuading management to implement accelerated cost cutting and restructuring. Proponents of increased shareholder participation say that, because of the conflicts of interest that arise in many management decisions, all the decision power should belong to shareholders. In this view, when shareholders have the power to decide, they delegate decisions about matters in which they lack sufficient information. Some challenge the idea increased shareholder power is a good idea, saying that shareholders lack adequate knowledge and skill to make effective decisions or that some shareholders may not have the firm’s best interests as their ultimate goal. For example, large institutional shareholders might try to inflate a firm’s stock price with short-term measures that actually reduced firm value, or shareholders might use their power to further a political, social, or environmental agenda at the expense of profits. Raviv and Harris used a mathematical model to investigate factors that might be overlooked in these arguments. Each group (management and shareholders) was assumed to act as if it were a single individual. Either group could control the decision, such as the size of a major investment or executive compensation. The group in control of a decision could make the decision itself or delegate it to the other party. Other assumptions were that management’s decisions would be biased away from maximizing share value and that both sides would have private information relevant to the decision. Raviv stresses that one important element of the model concerns communication: “If I know something, I might be able to communicate it to you, but the communication is not perfect or complete. I know that you are biased, so I communicate the information with a twist. The model accounts for that.” The Primacy of InformationThe researchers found that if shareholders have no private information, they will delegate the decision to management as long as management’s private information is sufficiently valuable that it outweighs the agency problem (the cost incurred when people entrusted to look after the interests of others use their power for their own benefit). However, the model did not suggest that shareholders should control all important corporate decisions. When shareholders have private information, they fail to delegate decisions to managers in some situations in which such delegation would increase share value. Raviv and Harris used the model to examine the possibility that shareholders may be not only ill informed but also overconfident in their ability to understand the issues involved in a decision. They also considered shareholders who want to use corporate resources for their own goals, such as environmentally friendly production techniques, wealth redistribution to workers, support for particular political candidates, or boycotts of certain products or countries. They determined that in both cases, shareholder control is optimal for some decisions. In their article in The Review of Financial Studies, they explain, “This is due, in part, to the fact that shareholder biases, due to either misperception or non-value-maximizing agendas, may improve communication from management to shareholders.” Real-World DecisionsIn their paper the researchers give several examples of how their findings apply to actual decisions. One is a decision about how much cash to distribute to shareholders. In this case management will likely have pertinent information not available to shareholders and shareholders will likely have little or no private information. It might seem obvious, then, that management should control this decision. However, the results from the model suggest just the opposite, supporting what activist shareholders are currently arguing. When it is time to replace a manager, both management and shareholders are likely to have information about the talent available, Raviv and Harris point out. Data from their model suggest that shareholder control of the decision maximizes share value regardless of the level of private benefits of control or the importance of the parties’ private information, as long as the two sides have information of similar importance. A third example is a decision about setting performance-based compensation. In this case, management’s information about the optimal compensation scheme is likely to be more important than shareholders’ information about low-level executives. On the other hand, for top executives, the importance of management’s information may be roughly comparable to that of shareholders’ information. The results from the model imply that, assuming similar agency costs for the two decisions, shareholder control is more likely to be optimal for top-level compensation decisions than for lower-level. Raviv and Harris conclude that it is disingenuous to protest that shareholders should not have decision-making authority because they lack information—shareholders can and do delegate decisions to management when necessary. On the other hand, even if shareholders seek to maximize firm value and can delegate decisions, they should not control all major decisions. Proponents of increased shareholder participation say that, because of the conflicts of interest that arise in many management decisions, all the decision power should belong to shareholders. In this view, when shareholders have the power to decide, they delegate decisions about matters in which they lack sufficient information. Some challenge the idea increased shareholder power is a good idea, saying that shareholders lack adequate knowledge and skill to make effective decisions or that some shareholders may not have the firm’s best interests as their ultimate goal. For example, large institutional shareholders might try to inflate a firm’s stock price with short-term measures that actually reduced firm value, or shareholders might use their power to further a political, social, or environmental agenda at the expense of profits. Raviv and Harris used a mathematical model to investigate factors that might be overlooked in these arguments. Each group (management and shareholders) was assumed to act as if it were a single individual. Either group could control the decision, such as the size of a major investment or executive compensation. The group in control of a decision could make the decision itself or delegate it to the other party. Other assumptions were that management’s decisions would be biased away from maximizing share value and that both sides would have private information relevant to the decision. Raviv stresses that one important element of the model concerns communication: “If I know something, I might be able to communicate it to you, but the communication is not perfect or complete. I know that you are biased, so I communicate the information with a twist. The model accounts for that.” The Primacy of InformationThe researchers found that if shareholders have no private information, they will delegate the decision to management as long as management’s private information is sufficiently valuable that it outweighs the agency problem (the cost incurred when people entrusted to look after the interests of others use their power for their own benefit). However, the model did not suggest that shareholders should control all important corporate decisions. When shareholders have private information, they fail to delegate decisions to managers in some situations in which such delegation would increase share value. Raviv and Harris used the model to examine the possibility that shareholders may be not only ill informed but also overconfident in their ability to understand the issues involved in a decision. They also considered shareholders who want to use corporate resources for their own goals, such as environmentally friendly production techniques, wealth redistribution to workers, support for particular political candidates, or boycotts of certain products or countries. They determined that in both cases, shareholder control is optimal for some decisions. In their article in The Review of Financial Studies, they explain, “This is due, in part, to the fact that shareholder biases, due to either misperception or non-value-maximizing agendas, may improve communication from management to shareholders.” Real-World DecisionsIn their paper the researchers give several examples of how their findings apply to actual decisions. One is a decision about how much cash to distribute to shareholders. In this case management will likely have pertinent information not available to shareholders and shareholders will likely have little or no private information. It might seem obvious, then, that management should control this decision. However, the results from the model suggest just the opposite, supporting what activist shareholders are currently arguing. When it is time to replace a manager, both management and shareholders are likely to have information about the talent available, Raviv and Harris point out. Data from their model suggest that shareholder control of the decision maximizes share value regardless of the level of private benefits of control or the importance of the parties’ private information, as long as the two sides have information of similar importance. A third example is a decision about setting performance-based compensation. In this case, management’s information about the optimal compensation scheme is likely to be more important than shareholders’ information about low-level executives. On the other hand, for top executives, the importance of management’s information may be roughly comparable to that of shareholders’ information. The results from the model imply that, assuming similar agency costs for the two decisions, shareholder control is more likely to be optimal for top-level compensation decisions than for lower-level. Raviv and Harris conclude that it is disingenuous to protest that shareholders should not have decision-making authority because they lack information—shareholders can and do delegate decisions to management when necessary. On the other hand, even if shareholders seek to maximize firm value and can delegate decisions, they should not control all major decisions. Featured Faculty About the Writer Beverly A. Caley, JD, is an independent writer based in Corvallis, Ore., who concentrates on business, legal, and science topics. About the Research Harris, Milton, and Artur Raviv. 2010. Control of corporate decisions: shareholders vs. management. The Review of Financial Studies 23(11): 4115–4147. Read the original Most Popular This Week

More in Finance & Accounting What are some mechanisms that encourage managers to act in best interests of shareholders?Compensation: Managers get paid for serving and working for the value maximization of shareholders. They receive bonuses, option payouts, or stocks additionally, which are directly related to the performance of the organization.

What are some of the forces that causes managers to act in the interest of shareholders?For example, a manager can be motivated to act in the shareholders' best interests through incentives such as performance-based compensation, direct influence by shareholders, the threat of firing, or the threat of takeovers.

Why might one expect managers to act in shareholders interest give some reasons?Managers would act in shareholders' interests because they have a legal duty to act in their interests. Managers may also receive compensation, either bonuses or stock and option payouts whose value is tied (roughly) to firm performance.

What can be done to ensure that managers pursue the interests of stockholders?Aligning Goals

Stockholders should take care to align their own goals with the goals of their managers. One of the simplest ways to do this is to pay managers partially in stock, making them stockholders themselves who have an interest in seeing the company succeed.

|

What are the factors that determine whether managers act in the best interest of stockholders?

zusammenhängende Posts

Urheberrechte © © 2024 berikutyang Inc.